Your credit score is a three-digit number that reflects your creditworthiness. It’s a vital component of your financial life, impacting everything from loan approvals to rent applications. Understanding how this number is calculated empowers you to make informed financial decisions. In this comprehensive guide, we’ll delve into the specifics of credit scores and explore strategies for improving them quickly and effectively.

A credit score is a numerical representation of your creditworthiness, essentially a summary of your borrowing history. Lenders use this score to assess your risk as a borrower. A higher credit score suggests a lower risk, which often translates to better loan terms and lower interest rates.

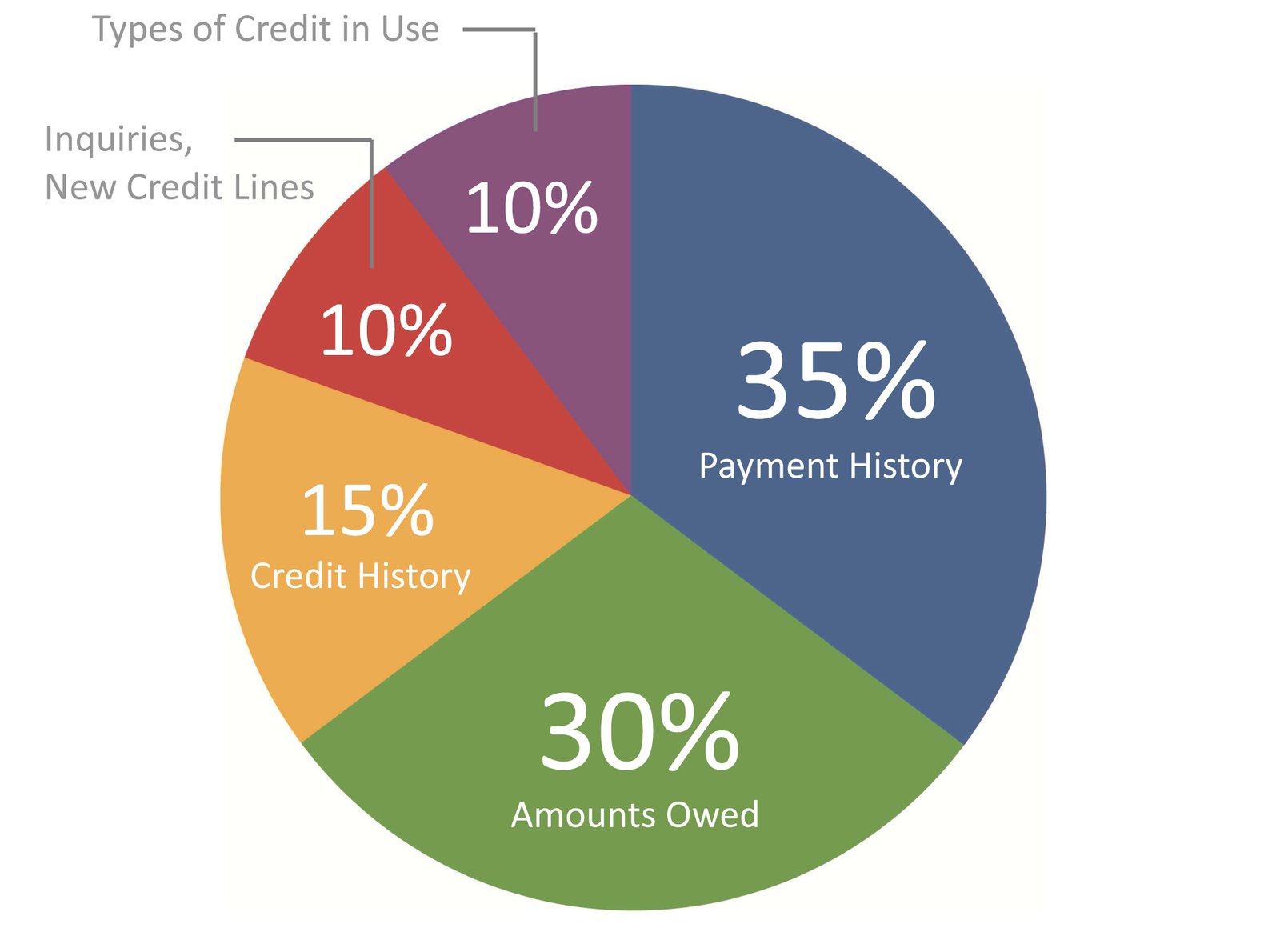

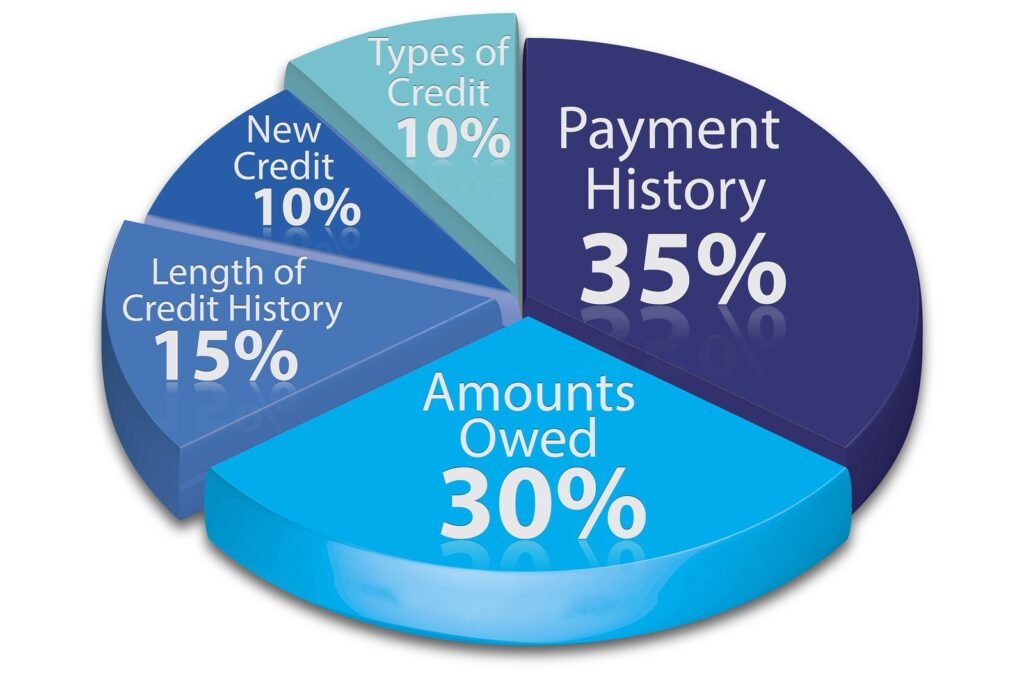

The calculation of a credit score isn’t arbitrary. Numerous factors contribute to the final number, and their relative weights vary depending on the specific credit scoring model used (e.g., FICO). These key factors include payment history, amounts owed, length of credit history, new credit, and types of credit.

Payment history holds significant weight in credit score calculations. Consistently making timely payments on your debts demonstrates responsible borrowing habits, resulting in a positive impact on your score. Late or missed payments can significantly damage your credit score, making it harder to secure loans or credit in the future.

The total amount of debt you have relative to your available credit (credit utilization) also plays a crucial role in shaping your credit score. Keeping your credit utilization low—ideally below 30%—is beneficial for maintaining a good credit score. High credit utilization indicates a higher risk of default, thus negatively affecting your score.

Related Post : Credit Card Mistakes You Need to Avoid

The length of your credit history is another important factor considered in credit score calculations. A longer credit history demonstrates a consistent record of responsible borrowing, strengthening your standing as a reliable borrower. A shorter history carries less weight and can potentially impact your score.

The presence of new credit accounts can also influence your score. While responsible use of new credit is beneficial, opening too many new accounts in a short period of time can potentially be perceived as high-risk.

Another factor is the types of credit you use. A diversified credit mix (credit cards, installment loans, mortgages) demonstrates your ability to handle different types of debt. A portfolio showcasing responsibility in various lending types can be helpful. Avoid relying solely on one type of credit.

Understanding these factors allows you to make informed choices about your finances. Taking proactive steps to manage your credit responsibly can significantly impact your creditworthiness. Taking care of your finances is an investment in yourself.

The most effective methods of improving your credit score rapidly include paying bills on time, ensuring low credit utilization, maintaining a long credit history, and avoiding applications for new credit too often. A significant factor for improvement is responsible debt management, and consistently meeting your financial obligations. This is an ongoing effort, and should be considered an important aspect of your life for financial prosperity and to ensure loan qualification for the future. How to Improve Your Credit Score Fast – [link to relevant article on improving credit score]. This article further details practical strategies for improving your score swiftly and responsibly. Using secured credit cards can also be a good strategy to build a credit history. For example [link to article on secured credit cards] further details this approach.

Understanding your credit score is crucial for financial success. By comprehending how it’s calculated and the factors that influence it, you can take proactive steps to improve your standing and unlock better financial opportunities. Remember, building a strong credit history takes time and consistent responsible financial behavior. If you need assistance, consulting a financial advisor can provide tailored guidance for your specific situation.

By

By