Planning for retirement is crucial, and understanding the nuances of retirement savings accounts is key. Two popular options are Roth IRAs and Traditional IRAs, each with its own set of benefits and drawbacks. This article dives deep into Roth IRA vs Traditional IRA, helping you discern which account optimal aligns with your financial objectives and tax situation.

Choosing the right retirement account can significantly impact your financial future. This guide offers a clear comparison of Roth IRAs and Traditional IRAs, outlining the key differences and helping you decide which might be the better fit for you.

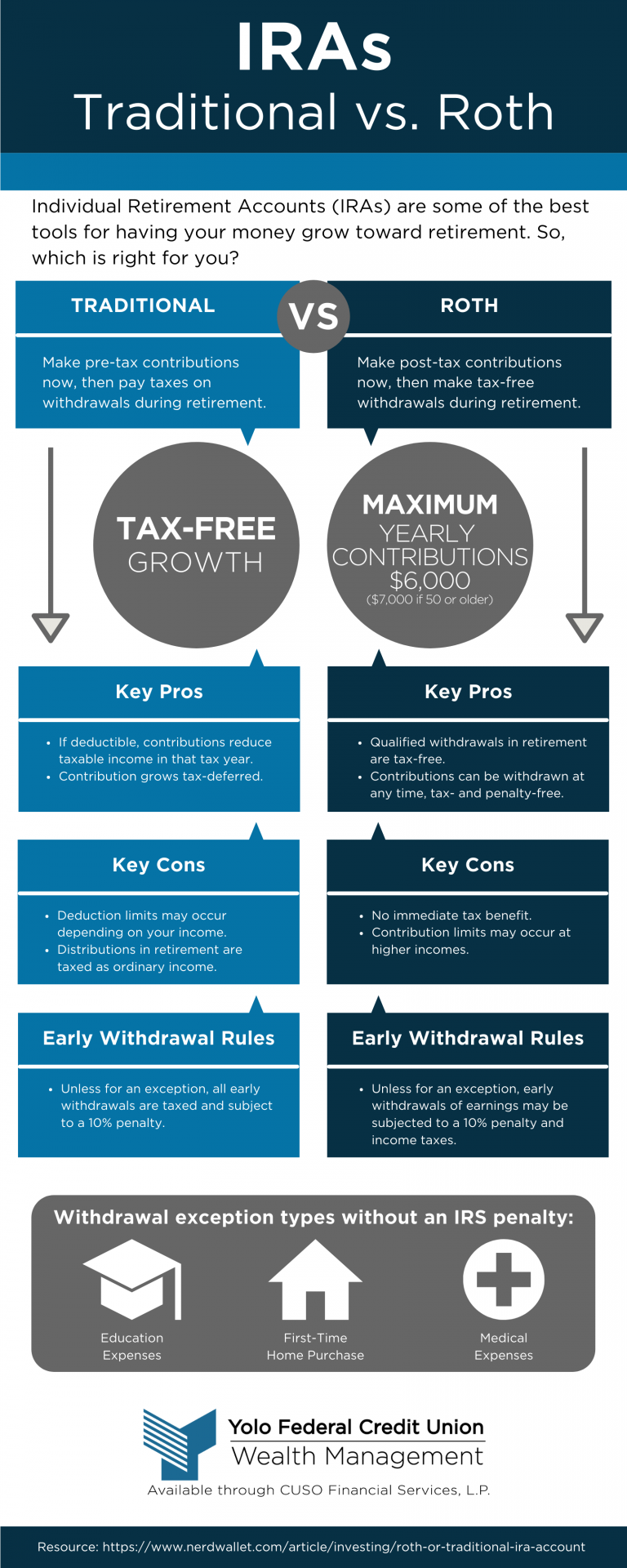

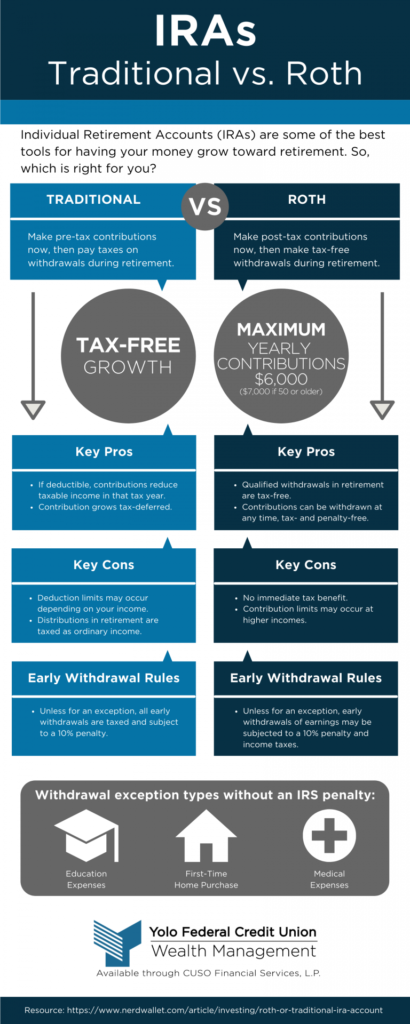

Both Roth IRAs and Traditional IRAs are tax-benefitd retirement savings accounts, designed to encourage saving for retirement. However, they differ significantly in how they affect your taxes now and in retirement.

Traditional IRA: Contributions may be tax-deductible in the year you make them, potentially lowering your current tax burden. However, withdrawals in retirement are taxed as ordinary income.

Roth IRA: Contributions aren’t tax-deductible, but qualified withdrawals in retirement are tax-complimentary. This means your withdrawals in retirement will be complimentary from income taxes.

Related Post : Best ETFs to Invest in 2024 for Steady Returns

Understanding the tax implications is paramount when choosing between these accounts.

Tax Deductibility Today: A significant difference lies in the immediate tax benefits. Traditional IRA contributions can reduce your taxable income in the year of contribution, potentially leading to substantial tax savings now. Conversely, Roth IRA contributions aren’t tax-deductible, meaning you won’t see a direct tax break this year.

Taxation in Retirement: This is where the real divergence comes into play. Traditional IRA withdrawals are taxed as ordinary income in retirement, while Roth IRA withdrawals are tax-complimentary. This means your potential tax burden is deferred with a Traditional IRA, and your retirement income is tax-complimentary with a Roth IRA.

Contribution Limits: Both accounts have annual contribution limits that are subject to change annually. Understanding these limits is crucial for maximizing your retirement savings.

Who might benefit from a Traditional IRA? Individuals in higher tax brackets now may find the present tax deduction of a Traditional IRA benefitous, potentially maximizing tax savings in their prime earning years. Additionally, those anticipating being in a lower tax bracket in retirement may find a Traditional IRA more beneficial. Learn more about calculating your current tax bracket by consulting our guide to [Link to Tax Bracket Guide] or other pertinent resources, so you can make an informed decision based on your projected future income. For those looking for immediate tax benefits, a Traditional IRA could be a good choice, but always carefully weigh the long-term implications against your future tax bracket in retirement. A consultation with a financial planner can offer valuable insights and personalized recommendations based on your specific circumstances and financial situation. You can also explore the intricacies of [link to Traditional IRA guide].

Who might benefit from a Roth IRA? Individuals anticipating being in a higher tax bracket in retirement might prefer a Roth IRA, as the tax-complimentary nature of withdrawals in retirement can offer a significant benefit in avoiding potential boosts in income tax obligations during retirement. In particular, high-income earners who project significant earnings in their retirement years often benefit from Roth IRAs. This is one example of how understanding your long-term financial objectives is vital when planning your retirement savings plan. For more insights, see our article on [Link to Roth IRA Guide]. Also, refer to [Link to High-income earners and retirement planning guide] for specific guidance on tax strategies tailored to higher earners and retirement planning. Consult a financial advisor to explore if a Roth IRA fits your individual financial circumstances and projected income levels.

Additional Considerations: Other facets to consider include the flexibility of both accounts and whether you anticipate needing access to funds during the accumulation stage. For details about [link to contribution limits], you can visit the IRS website for the most up-to-date information.

Ultimately, the optimal choice between a Roth IRA and a Traditional IRA depends on your individual financial situation, tax bracket, and retirement objectives. Carefully consider the pros and cons of each, and consult with a financial advisor to make an informed decision that aligns with your long-term financial plan.

By

By