Introduction to Budgeting

Budgeting is the systematic process of creating a plan to manage one’s financial resources. It involves tracking income and expenses to ensure that individuals can meet their financial obligations while also saving for the future. The primary purpose of budgeting is to gain a clearer understanding of one’s financial situation and to facilitate informed decision-making regarding expenditures. For beginners, adopting a budget can be a game-changer, enabling them to lay a solid foundation for their financial health.

Establishing a budget serves several key purposes. Firstly, it allows individuals to identify their income sources and understand their spending habits. By meticulously recording and categorizing expenditures, individuals can pinpoint areas where they may be overspending. This increased awareness can aid in making conscious choices that promote financial stability. Additionally, effective budgeting can help in setting and achieving financial goals, whether short-term, such as saving for a vacation, or long-term, such as preparing for retirement.

The importance of budgeting cannot be overstated, especially for those just starting out on their financial journey. A well-structured budget acts as a roadmap, guiding individuals toward their financial objectives while keeping them accountable for their spending. It fosters discipline and encourages mindful financial practices, which are essential skills for maintaining financial health.

Moreover, a budget can serve as a valuable tool in managing unexpected expenses or financial emergencies. By allocating funds for discretionary spending and savings, individuals can create a buffer that offers security and flexibility. In this way, budgeting not only aids in daily financial management but also contributes to long-term financial wellness.

Tip 1: Track Your Income and Expenses

Commencing a budgeting journey necessitates a foundational step: tracking your income and expenses. Becoming aware of the flow of money is crucial, as it lays the groundwork for effective financial management. Various methods can facilitate the monitoring of these financial elements, empowering individuals to make informed decisions.

One of the most straightforward approaches to tracking finances is using spreadsheets. Programs like Microsoft Excel or Google Sheets allow users to set up custom templates that accommodate personal needs. Users can create categories for different income sources and expenses, ensuring comprehensive documentation. This method provides flexibility and the ability to perform calculations automatically, making it easier to analyze trends over time.

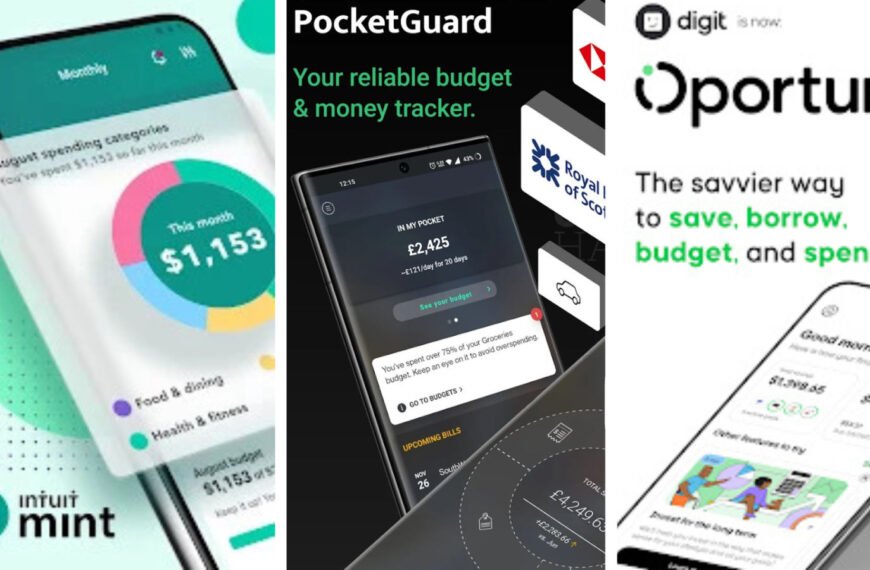

Alternatively, utilizing budgeting apps has gained popularity among many due to their convenience and accessibility. Applications such as Mint, YNAB (You Need A Budget), and PocketGuard sync with bank accounts, automatically categorizing transactions and providing real-time insights into spending habits. These apps often include features to set financial goals and alerts for overspending, aiding in maintaining accountability.

For those who prefer a hands-on approach, pen and paper remains a viable option. Keeping a physical journal dedicated to tracking income and expenses can foster a deeper awareness of financial habits. While it may require more effort than digital tools, writing by hand can enhance memory retention and engagement with your finances.

Regardless of the method chosen, the key lies in consistency and commitment to monitor income and expenses regularly. This practice enables individuals to identify patterns, highlight areas for potential savings, and ensure that spending aligns with financial goals. By establishing a habit of tracking where money flows, beginners can pave the way for a sound budgeting plan that supports long-term fiscal health.

Tip 2: Set Clear Financial Goals

Establishing specific and measurable financial goals is a crucial step in effective budgeting. Without a clear direction, managing finances can seem overwhelming, leading to haphazard spending and a lack of progress. Financial goals can be categorized into short-term and long-term objectives, both of which play significant roles in a holistic budgeting strategy.

Short-term goals typically span a duration of less than one year and may include targets such as saving for a vacation, building an emergency fund, or paying off credit card debt. These goals are often tangible and immediate, making them easier to track and achieve within a shorter time frame. Setting specific amounts to save or allocate each month toward these short-term goals can help create a structured plan that aligns with your overall budget.

In contrast, long-term goals involve financial objectives that take several years to achieve. Examples include saving for retirement, purchasing a home, or funding a child’s education. These targets require careful planning since they may involve larger sums of money and extended saving periods. Establishing a timeline and budget for reaching long-term goals is essential, as it ensures continued motivation and accountability in your budgeting efforts.

To create effective financial goals, it is vital to ensure that they are SMART: Specific, Measurable, Achievable, Relevant, and Time-bound. By applying this framework, individuals can establish realistic targets that will steer their budgeting practices. Importantly, aligning your budgeting strategies with these goals enhances your ability to monitor progress over time, making necessary adjustments as needed. This alignment not only increases the likelihood of achieving financial success but also fosters a sense of discipline and commitment to your overall financial health.

Tip 3: Create a Realistic Budget Plan

Creating a realistic budget plan is a crucial step for anyone beginning their financial journey. A well-structured budget allows individuals to understand their income, expenses, and savings potential, leading to informed financial decisions. One fundamental approach to budgeting is the 50/30/20 rule, which divides after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment. This method provides a clear framework that simplifies the budgeting process, ensuring that essential expenses are covered while still allowing for discretionary spending and future financial goals.

When crafting a budget plan, it is essential to consider both fixed and variable expenses. Fixed expenses, such as rent or mortgage payments, utilities, and insurance, remain constant each month, making them easier to allocate within a budget. In contrast, variable expenses, like groceries, dining out, and entertainment, may fluctuate, requiring careful tracking and adjustment to align with overall financial goals. By meticulously categorizing these expenses, individuals can create a comprehensive view of their financial landscape, aiding in realistic budgeting.

Additionally, it is vital that the budget remains manageable and flexible. Beginners should avoid overly restrictive plans that could lead to frustration or abandonment of their budget. Setting achievable goals and regularly reviewing and adjusting the budget based on changing circumstances not only fosters improvement but also builds financial confidence. Engaging tools such as budgeting apps or spreadsheets can facilitate this process and provide a visual representation of one’s financial health. Ultimately, dedicated effort and persistence in adhering to a budget plan can pave the path towards financial stability and achievement of one’s monetary aspirations.

Tip 4: Monitor and Adjust Your Budget Regularly

Effective budgeting is not a one-time task; it requires continual monitoring and adjustments to align with changing circumstances. Regularly reviewing your budget allows you to track your progress towards financial goals and make necessary changes based on new information or shifting priorities. This approach ensures that your financial plan remains relevant and effective over time.

Begin by setting up a schedule for budget reviews—this could be weekly, monthly, or quarterly, depending on your financial situation. During these reviews, take the time to analyze your spending patterns, savings progress, and financial commitments. Assess whether you are on track to achieve your goals, such as saving for a vacation, paying off debt, or building an emergency fund. If you find discrepancies between your planned expenses and actual spending, it may be time to adjust your budget accordingly.

Flexibility is an essential characteristic of a successful budgeting strategy. Life can bring unexpected circumstances, such as job changes, medical expenses, or shifts in family needs, all of which may require you to reassess your financial plan. Being open to revising your budget when faced with such changes can help you maintain control over your finances and navigate challenges more effectively.

Furthermore, consider incorporating tracking tools or apps to streamline the monitoring process. These tools can provide clear visuals of your spending habits and help identify areas where adjustments may be necessary. By analyzing trends in your finances, you can make more informed decisions about where to allocate resources. Ultimately, regular monitoring and adjustments ensure that your budgeting remains a dynamic process, equipped to support your evolving financial journey.

Tip 5: Find Ways to Save Money

Saving money is an essential part of effective budgeting, and there are several practical strategies that individuals can adopt to reduce expenses without compromising their lifestyle. One of the first steps in identifying areas for savings is to conduct a thorough review of monthly expenditures. This review should include all recurring expenses such as subscriptions, memberships, and utility bills.

Cutting unnecessary expenses can dramatically impact one’s financial situation. For instance, assessing subscription services can highlight options that are rarely utilized, allowing for cancellation without a second thought. Similarly, reviewing dining habits can uncover excessive spending on takeout or restaurant meals, which can be replaced with home-cooked alternatives that are often healthier and more economical.

Another effective strategy to save money involves taking advantage of discounts and coupons. Many retailers and service providers offer seasonal promotions or loyalty programs that can significantly reduce costs. Utilizing websites and apps that aggregate coupons not only simplifies the process of finding deals but also encourages smarter purchasing decisions. Additionally, it is beneficial to look into cashback options, whether through credit cards or dedicated savings apps, which provide a percentage of money back on purchases.

Making informed purchasing decisions can yield substantial savings over time. This may include waiting for sales or exploring alternative brands that deliver similar quality at a lower cost. It is also advisable to create a shopping list before making purchases. This strategy minimizes impulse buying and helps maintain budgetary discipline.

Through these efforts, individuals can strategically find ways to save money, thus creating more room in their budget while still enjoying the lifestyle they desire. With consistency in applying these money-saving tips, anyone can foster a more sustainable financial future.

Common Budgeting Mistakes to Avoid

Budgeting can be a daunting task for beginners, especially when it comes to avoiding common pitfalls that may derail financial goals. One of the most frequent mistakes is underestimating expenses. Many individuals fail to accurately assess their monthly costs, leading to a budget that does not truly reflect reality. To mitigate this issue, it is crucial to review past spending habits and consider fixed costs such as rent, utilities, and insurance, as well as variable costs like groceries and entertainment. Maintaining a comprehensive list of all expected expenses will provide a clearer picture of financial obligations.

Another common oversight is neglecting irregular costs. Beginners often focus only on recurring monthly expenses and, as a result, may be unprepared for additional expenses that arise—such as car maintenance or holiday gifts. Establishing a sinking fund for irregular expenses can help ensure that these costs are accounted for in the budgeting process. This approach allows individuals to set aside a specific amount each month to cover non-monthly expenses, therefore avoiding financial strain when they inevitably arise.

Consistency is another critical aspect often overlooked by beginners. Not tracking spending regularly can lead to a lack of awareness about financial habits, ultimately resulting in overspending. It is essential to maintain a weekly or monthly review of expenses to understand where money is being allocated. Utilizing budgeting tools or applications can enhance this tracking method, providing insights and allowing for better financial management. By developing the habit of consistently monitoring expenditures, individuals can avoid falling into the trap of miscalculating their budget.

Through awareness and practice, it is possible to sidestep these common budgeting mistakes. Developing a realistic budget and staying attentive to irregular costs will ultimately lead to healthier financial habits for beginners.

Tools and Resources for Budgeting

For beginners venturing into the world of budgeting, utilizing the right tools and resources is paramount. A variety of budgeting apps, websites, and literature are available to simplify the process of managing personal finances effectively. These resources can guide individuals in their quest to establish a budget, track expenses, and attain financial goals.

One of the most recommended budgeting tools is mobile applications. Apps such as Mint and YNAB (You Need a Budget) facilitate financial oversight by allowing users to link their bank accounts, categorize expenditures, and analyze spending habits. Mint automatically organizes transactions and provides insights into spending trends, while YNAB emphasizes proactive budgeting by encouraging users to allocate every dollar to a task, thus promoting financial discipline.

In addition to mobile applications, websites like Personal Capital and BudgetTracker offer comprehensive budgeting solutions. Personal Capital combines budgeting with investment tracking, offering a holistic view of one’s financial landscape, which can be particularly beneficial for those starting to invest and save for retirement. BudgetTracker, on the other hand, allows individuals to manually input their expenses and income, providing an unobstructed view of their financial progress.

Literature also plays a significant role in shaping budgeting knowledge. Books such as “The Total Money Makeover” by Dave Ramsey and “The Budgeting Habit” by S.J. Scott provide practical advice for effective budgeting practices. These resources delve into strategies for maintaining a budget, saving money, and managing debt while encouraging a mindset that values financial stability.

By exploring these various budgeting tools and resources, beginners can enhance their financial literacy and develop a personalized budgeting system that suits their unique needs and preferences. With the right approach, anyone can gain control over their finances, paving the way for a secure financial future.

The Importance of Maintaining a Positive Mindset

When embarking on the journey of budgeting, it is crucial to recognize the significant impact that a positive mindset can have on the overall experience. Approaching budgeting with an optimistic outlook not only enhances motivation but also fosters resilience against the inevitable challenges that may arise. A positive perspective can transform budgeting from a daunting task into an achievable goal, providing individuals with the confidence necessary to manage their finances effectively.

Staying motivated during the budgeting process is essential for long-term success. Setting realistic financial goals is one effective strategy to maintain motivation. These goals should be specific, measurable, attainable, relevant, and time-bound (SMART). By breaking down larger financial objectives into manageable steps, individuals can create a clear roadmap to follow. This approach not only alleviates feelings of overwhelm but also allows for a series of small victories to be celebrated along the way, reinforcing a positive mindset.

Celebrating these small victories is instrumental in maintaining enthusiasm for budgeting. Each time a financial goal is accomplished, whether it’s saving a set amount of money or successfully sticking to a budget for the month, individuals should take a moment to appreciate their success. This practice reinforces the idea that budgeting is a journey filled with incremental progress rather than an insurmountable hurdle. Additionally, positive reinforcement can help integrate budgeting practices into daily life, making it an integral part of one’s routine.

In summary, a positive mindset is critical in the budgeting process. By focusing on achievable goals and celebrating small milestones, individuals can cultivate a healthy relationship with budgeting. This not only aids in effective financial management but also enhances overall well-being, setting the foundation for a stable financial future.

Conclusion and Next Steps

In summary, effective budgeting is an essential skill that can significantly impact one’s financial well-being. Throughout this blog post, we have explored five simple yet powerful budgeting tips designed specifically for beginners. These tips focus on setting clear financial goals, tracking expenses diligently, creating a realistic budget plan, being flexible with adjustments, and regularly reviewing financial progress. Each of these steps plays a crucial role in establishing a strong foundation for personal finance management.

As you embark on your budgeting journey, it is vital to recognize that the initial stages may pose some challenges. However, it is important to approach these challenges with patience and persistence. The key to mastering budgeting lies in consistent practice and adaptation to your unique financial situation. By regularly revisiting your budget, you can identify areas that may require adjustments, ensuring that your financial plan remains effective over time.

To implement your budgeting plan, begin by setting aside a dedicated time each week or month to review your finances and make necessary changes. This regular check-in will enhance your engagement with your budget, making it a more tangible part of your financial lifestyle. Furthermore, consider utilizing budgeting tools or apps that can simplify the process, help you visualize your spending habits, and maintain motivation.

As you continue to refine your budgeting skills, remember that the ultimate goal is not solely about managing expenses but also about achieving your broader financial aspirations. Whether it’s saving for a vacation, paying off debt, or securing your future, each small step you take toward effective budgeting contributes to your long-term financial success. Ultimately, with diligence and commitment, budgeting will evolve from a challenging task into a rewarding routine that empowers you to make informed financial decisions.

By

By